Smart Savings: How to Plan and Save for Big Purchases Without Going Broke

MANAGING MONEY

5 min read

Understanding the Importance of Saving for Big Purchases

Saving for big purchases is a fundamental aspect of sound financial planning. It enables individuals to acquire significant items or experiences without incurring debt, fostering long-term financial health and stability. Unlike financing, which typically involves borrowing funds and paying interest, saving allows consumers to pay for purchases upfront, ultimately leading to considerable savings over time. By prioritizing savings, individuals can avoid the pitfalls associated with debt, such as high interest rates and financial stress.

The practice of saving for major expenses empowers consumers to make informed purchasing decisions. When individuals save diligently for a significant item, they are more likely to conduct thorough research and compare options, ensuring that they choose the best product for their needs and budget. This thoughtful approach often results in greater satisfaction with the purchase and can lead to higher quality items that last longer, ultimately providing better value.

Setting financial goals and saving towards them creates a sense of accomplishment and discipline. It fosters a proactive attitude towards personal finance, encouraging individuals to track their savings progress and adjust their strategies as necessary. For instance, someone saving for a new car may start a dedicated savings account, setting aside a portion of their income each month. Over time, this effort not only brings them closer to their goal but also instills a habit of responsible financial management.

Real-life examples of effective savings strategies are abundant. Many individuals successfully save for major expenses, like home purchases or vacations, by establishing clear goals and adhering to structured savings plans. These experiences serve as motivation for others who may still rely on financing, demonstrating that with determination and planning, significant savings are achievable. Therefore, understanding the importance of saving for big purchases can significantly alter one’s financial trajectory, leading to a more secure and fulfilling future.

Setting Realistic Goals

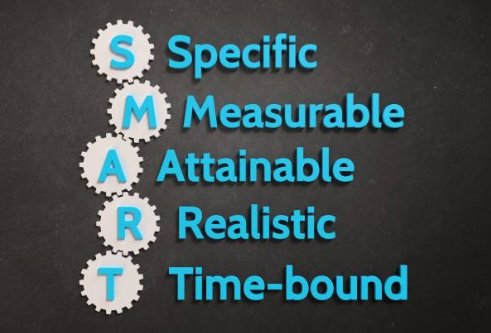

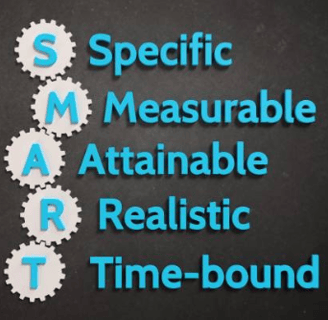

Establishing realistic goals is a crucial step in the process of planning and saving for significant purchases. Whether you are aiming to acquire a new vehicle, fund an unforgettable vacation, or invest in a major home appliance, recognizing and prioritizing these goals is essential. Start by assessing what you genuinely need versus what you desire. This distinction will help to streamline your focus and ensure that your financial resources are allocated effectively.

Begin by creating a list of potential big purchases. Each item should be evaluated in terms of its necessity, practicality, and long-term benefits. Following this, it is vital to delve into the financial aspects by estimating the total cost associated with each purchase. This examination should include not just the initial outlay but also other expenditures such as maintenance, insurance, and any other ongoing costs that may arise after the purchase. A comprehensive understanding of these financial obligations will help guide your decision-making process.

Once you have identified your priorities and assessed the costs, it is time to set a realistic timeline for saving. Consider how quickly you would like to make the purchase and then outline the monthly savings required to reach that goal within your timeframe. To enhance this process, breaking down larger objectives into smaller, more manageable short-term goals can significantly augment motivation and progress. Rather than being overwhelmed by a large sum, focusing on accumulating smaller amounts can create a sense of achievement, propelling you further toward your ultimate goal.

Thoughtful reflection on your big purchase needs, coupled with strategic planning for both costs and timeframes, can greatly facilitate a successful savings journey. This structured approach will not only help you attain your desired acquisition but also maintain financial stability throughout the process.

Effective Savings Strategies

Building a robust savings strategy is essential for achieving significant financial goals, especially when planning for substantial purchases. One effective approach is to create a dedicated savings plan tailored to your specific objectives. Start by determining the total amount needed for your upcoming purchase and establish a timeline for when you aim to achieve this goal. By breaking down the total amount into manageable monthly savings, you can monitor your progress effectively. Setting clear milestones can also enhance motivation, keeping you focused on your financial targets.

Utilizing automated savings plugins is an excellent way to streamline your savings efforts. Many banks and financial institutions offer tools that automatically transfer a predetermined amount from your checking account to your savings account at regular intervals. This “pay yourself first” approach helps you save consistently without the temptation to spend the funds. Such automation not only aids in discipline but also allows you to allocate funds with minimal effort on your part.

Setting up a high-yield savings account is another smart strategy. Unlike traditional savings accounts, these accounts typically offer higher interest rates, enabling your savings to grow more significantly over time. This increased growth can be particularly advantageous when planning for large expenses, as the additional interest can accelerate the pace at which you reach your financial goals. Pairing this with effective budgeting apps that track your spending can further enhance your ability to save. Many budgeting tools allow you to categorize expenses and identify areas where you can cut unnecessary costs, creating a clearer path to achieving your savings goals.

Adopting simple lifestyle changes to reduce expenses—such as meal prepping, finding cheaper alternatives, or lowering subscription services—can significantly influence your savings rate. By implementing these practical strategies and utilizing available tools, you can effectively build your savings and ensure you are well-prepared for your upcoming purchases.

Avoiding Financial Strain

Maintaining a commitment to a saving plan can be challenging, especially when unexpected financial challenges arise. One effective strategy to avoid financial strain is to incorporate flexibility into your budget. Initially, set a savings target and timeline, but remain open to adjusting these goals based on changing circumstances. If you encounter an emergency expense, for instance, consider reallocating resources temporarily rather than abandoning your saving efforts altogether. This adaptive approach ensures that you can still work towards your objectives without feeling overwhelmed.

In addition to budgeting flexibility, it is essential to develop coping mechanisms to handle unforeseen financial challenges. Start by establishing an emergency fund that can serve as a financial cushion during difficult times. This fund should be separate from your primary savings goal but still easily accessible. Having this backup can enable you to address urgent expenses without derailing your progress toward larger purchases. Setting realistic expectations about your saving journey, including anticipating potential setbacks, will also prepare you to respond more effectively when obstacles arise.

From a psychological standpoint, maintaining motivation is crucial for staying committed to your saving plan. It can be beneficial to break your larger goal into smaller milestones, allowing you to celebrate incremental achievements along the way. These milestones not only boost your morale but also provide a clear sense of progress. Additionally, consider involving friends or family members in your saving journey; their support can create accountability and encouragement. Share your goals with them, as this can enhance both motivation and commitment.

By integrating flexibility into your budgeting, creating a financial safety net, and fostering a supportive environment, you can avoid financial strain while diligently working toward your savings goals. Staying focused on your long-term objectives can lead to financial security without compromising your overall wellbeing.