The Power of Compound Interest: How It Can Grow Your Wealth

INVESTMENT STRATEGIES

9 min read

Understanding Compound Interest

Compound interest is a fundamental concept in finance that refers to the process of earning interest on both the original principal and the interest that has previously been added. This contrasts sharply with simple interest, which is calculated solely on the principal amount. A clear comprehension of compound interest is essential for maximizing wealth and making informed investment decisions.

To illustrate, let us consider an example. Suppose you invest $1,000 at an annual interest rate of 5%. With simple interest, you would earn $50 each year, resulting in a total accumulation of $1,250 after five years. However, with compound interest, the scenario changes significantly. In the first year, you would earn $50 in interest, bringing your total to $1,050. In the second year, you earn interest not just on the original $1,000, but also on the $50 of interest from the first year, yielding $52.50, resulting in a total of $1,102.50. This compounding effect continues each year, leading to a far greater amount over time, where your total would surpass $1,276 after five years.

The significance of time cannot be overstated when it comes to compound interest. The longer the time frame, the greater the amount of interest earned on the accumulated principal and previous interest. This exponential growth is often referred to as the "time value of money." For instance, if one were to invest early, even small amounts can grow considerably larger due to the power of compounding. Therefore, understanding how compound interest operates allows individuals to plan better for their financial futures, emphasizing the necessity of starting to invest as early as possible.

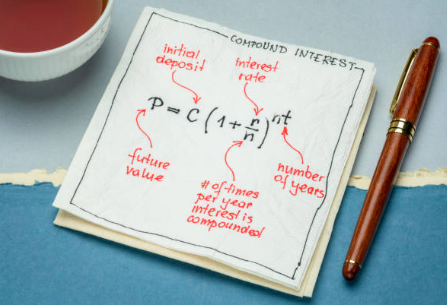

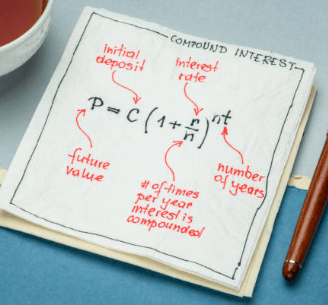

The Formula Behind Compound Interest

Compound interest is a financial concept that plays a critical role in wealth accumulation. The fundamental formula for calculating compound interest is:

A = P (1 + r/n)^(nt)

Where:

A = the future value of the investment/loan, including interest

P = the principal investment amount (the initial deposit or loan amount)

r = the annual interest rate (decimal)

n = the number of times that interest is compounded per year

t = the number of years the money is invested or borrowed

Understanding this formula is essential for anyone looking to grow their wealth through investments. Let's break it down further. The principal amount, represented by P, is where the growth begins. The interest rate r is crucial as it determines how much your investment will earn over time. The compounding frequency, captured by n, indicates how often interest is applied to the principal. The time period t magnifies the effect of compounding; the longer the money is allowed to grow, the more significant the effect overall.

For instance, consider an initial investment of $1,000 with an annual interest rate of 5%, compounded quarterly for 10 years. Plugging the values into the formula:

A = 1000 (1 + 0.05/4)^(4*10)

By calculating this, one would find that the future value of the investment grows to approximately $1,647.01. This example demonstrates the power of compound interest and the importance of time and frequency of compounding in maximizing returns. Moreover, it emphasizes the efficacy of starting early with investments to benefit from the exponential growth that compound interest facilitates.

The Effects of Time on Compound Interest

The duration of an investment plays a crucial role in the growth of wealth through compound interest. As time progresses, the effects of compounding become more pronounced, leading to significant financial gains. This relationship can be understood by examining various investment periods and how they affect overall wealth accumulation. The essence of compound interest lies in its ability to generate earnings on both the initial principal and the accumulated interest from previous periods. This results in what is often referred to as the "snowball effect," where growth accelerates over time.

For example, consider two individuals who invest the same amount of money at identical interest rates. The first person, Alice, invests $1,000 and leaves it untouched for 30 years, while her friend Bob invests the same $1,000 but only for 15 years. Assuming an annual interest rate of 5%, Alice’s investment will grow to approximately $4,321, while Bob's will amount to about $2,078. This stark contrast highlights the significance of time; by allowing an investment to mature over a longer period, one can harness the full potential of compounding.

Furthermore, starting early can lead to exponential growth due to the extended period of compounding. For young investors, even small contributions can accumulate into substantial wealth over decades. The earlier one begins investing, the longer the money has to grow. The impact of even just a few more years of compounding can be substantial, emphasizing the importance of making informed investment decisions early in life.

In essence, the duration of an investment is a pivotal factor in maximizing wealth through compound interest. By understanding and acknowledging the effects of time, individuals can make strategic decisions that enhance their financial futures. This strategy not only fosters patience but also encourages a long-term perspective on investments, which can ultimately lead to a more prosperous outcome.

Compounding Frequency: Monthly vs Annually

Understanding the nuances of compounding frequency is crucial for those looking to maximize their investments. The term "compounding frequency" refers to how often the interest is calculated and added to the principal balance of an investment or savings account. The main compounding intervals are annually, semi-annually, quarterly, and monthly. Each frequency can profoundly affect the amount of accumulated wealth over time.

When comparing annual and monthly compounding, the difference becomes apparent through practical examples. For instance, if one invests $1,000 at an interest rate of 5% compounded annually, after 10 years, the investment would grow to approximately $1,628.89. Conversely, if the same $1,000 investment is compounded monthly at the same interest rate, the total wealth after the same period increases to around $1,648.73. This demonstrates that even slight adjustments in compounding frequency can yield differing results.

Next, looking at semi-annual and quarterly compounding further illustrates the impact of frequency. If the initial investment of $1,000 is compounded semi-annually at a 5% interest rate, it would amount to approximately $1,634.88 after ten years. On the other hand, with quarterly compounding, the total reaches about $1,643.62. It is clear, then, that more frequent compounding intervals enhance the growth of wealth significantly. The reason behind this is simple: interest is calculated and added to the principal more often, which leads to interest being earned on interest sooner than with less frequent compounding.

The choice between compounding frequencies matters. Those making investment decisions should factor in the compounding frequency as a vital criterion, as it can bring about substantial differences in returns over time. The clear message is that, in the world of investment, the more frequently interest compounds, the greater the accumulation of wealth, thus unlocking the true potential of compound interest.

Real-Life Applications: Compound Interest in Investments

Compound interest is a powerful concept that can significantly influence investment outcomes. It operates on the principle of earning interest on both the principal amount and the accumulated interest from previous periods. This characteristic makes it especially beneficial for long-term investments where wealth can grow exponentially over time. Many investors leverage compound interest through various investment vehicles, including stock market investments, retirement accounts, and savings accounts.

In the stock market, investors can harness the power of compound interest through reinvestment of dividends. For instance, a company that provides a dividend yield of 4% allows investors to reinvest those dividends to purchase more shares. Over time, this reinvestment mechanism can lead to substantial growth in total returns, particularly when compounded over several years. Historical data supports this, indicating that the S&P 500, for example, has delivered average annual returns of approximately 10% over the long term when including reinvested dividends.

Retirement accounts such as 401(k)s and Individual Retirement Accounts (IRAs) are other prime examples of effective compound interest applications. These accounts often allow contributions to grow tax-deferred. As contributions persist and compounded earnings accrue, the end value at retirement significantly surpasses the total amounts contributed. For instance, an individual who starts saving $200 a month at age 25 can accumulate over $1 million by retirement age if the account grows at an average annual interest rate of 7%.

Traditional savings accounts can utilize compound interest to enhance personal savings strategies. Even though interest rates may be lower compared to investment accounts, the security they provide can be appealing. Monthly compounding in savings accounts means that every deposit generates interest, compounding period after period, leading to gradual wealth growth.

Compound interest can be a formidable tool when applied correctly across various investment vehicles. By understanding and leveraging its principles in stock markets, retirement accounts, and savings accounts, individuals can achieve significant long-term financial growth.

Common Misconceptions About Compound Interest

Compound interest is often misrepresented, leading to misunderstandings that can hinder financial decision-making. One prevalent myth is that compound interest guarantees high returns. While it is true that compounding can amplify the growth of investments over time, it is essential to recognize that returns are also influenced by various factors, including market fluctuations and economic conditions. Thus, one should not assume that compounding alone will yield exceptional profits without considering these external elements.

Another common misconception is the belief that fees have little impact on compound interest. In reality, even small fees can significantly erode investment gains when compounded over time. For instance, a 1% annual fee on a long-term investment can result in thousands of dollars in lost growth. Therefore, it is vital for investors to scrutinize fee structures associated with their investment vehicles, as these can dramatically affect the compounding effect.

Furthermore, it is essential to differentiate between simple interest and compound interest. Simple interest is calculated solely on the principal amount, while compound interest takes into account both the principal and the accumulated interest from previous periods. This distinction is often overlooked, leading to underestimations of potential earnings. Understanding how interest compounds over regular intervals can help investors appreciate the long-term benefits of their investments.

Many individuals mistakenly believe that compounding is only beneficial in the long term. While it is true that the benefits of compounding magnify with time, it is also effective in shorter investment horizons. Starting early, even with modest amounts, can lead to substantial growth due to the exponential nature of compound interest. By correcting these misconceptions, investors can harness the full potential of compound interest in wealth accumulation.

Start Harnessing the Power of Compound Interest Today

To fully leverage the benefits of compound interest and facilitate the growth of personal wealth, it is essential to implement practical strategies that align with financial goals. One fundamental step is to start by establishing retirement accounts, such as an Individual Retirement Account (IRA) or a 401(k). These accounts not only provide tax advantages but also allow your investments to grow exponentially over time due to the compounding effect. Contributing consistently to these accounts, even in small amounts, can lead to substantial growth over the years.

Creating a well-structured savings plan is another effective method to harness compound interest. This plan should outline monthly contributions to a high-yield savings account or money market account, which allows for interest to accumulate regularly. The emphasis should be on automating these contributions, ensuring that a portion of income is allocated towards saving each month. This habitual saving maximizes the compounding effect by adding new funds that can also generate interest.

Additionally, selecting suitable investment products is crucial in maximizing the impact of compound interest. Consider diversifying investments in a mix of stocks, bonds, and mutual funds, as these can yield varying rates of return. Equity investments, in particular, tend to offer higher returns over longer periods, thereby enhancing the compounding process. Always assess your risk tolerance and investment horizon before making decisions, as these factors significantly influence potential gains.

The key to harnessing the power of compound interest lies in starting as early as possible. The sooner one begins to save and invest, the more one can benefit from the relentless nature of compounding. Time is a potent ally in wealth accumulation, and taking control of your financial future today can lead to a more secure and prosperous tomorrow. Seize the opportunity to implement these strategies and watch your wealth grow through the magic of compound interest.